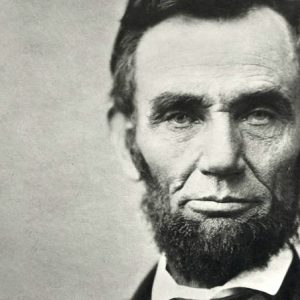

President Dwight Eisenhower and President Abraham Lincoln share something unusual in common. Neither had the support of family or friends when they ran for president.

No one in Lincoln’s family voted for him. And no one in Eisenhower’s home town of Denison, Texas voted for him. Though both lacked the moral support of family and friends, both won their presidential elections.

Lincoln and Eisenhower’s situations reminded me of something I learned decades ago.It’s more difficult for you to win over family and friends than the general public. A pastor was the first to warn me of this. He explained, “Your family remember how you acted before you became a follower of Jesus Christ. They’re going to be skeptical that you can change.”

The same attitude is often exhibited by your boss. “You can’t have any good ideas. You work for us.”

Good news! Lack of support from family, friends or bosses does not dictate your fate!

Lincoln and Eisenhower won because they sold big ideas not themselves. Lincoln promoted the end of slavery. Eisenhower promised to stand up to the communists as commander-in-chief.

Are you feeling like no one believes in you? Learn from Lincoln and Eisenhower. Identify something bigger than yourself. Something of importance that will add value to lots of people. The acceptance and appeal of that one big idea will raise your measure in everyone’s eyes.

My story

In 1985 a senior leader from Motorola HQ stopped me in mid-presentation, looked at my boss and said, “Don’t include anyone from accounting at quarterly operational reviews in the future. I only want to hear from people who can improve results, not report them.”

The leader did not believe in me. I could have gotten mad. Or I could have quit. But instead I sought out a better way to account for costs and improve decision-making. I found it. It was new. It’s called Activity-Based Costing (ABC). Finding and implementing that improved method resulted in Motorola’s leadership offering me a promotion in 1986. I turned it down, however, because my finding ABC opened even better career opportunities.

Your story

Find and promote something bigger than yourself and then people will believe in you.

]]>

Does your cost system need to be precise? Probably not.

Does it need to be accurate. Yes!

What’s the difference? The four pictures above begin to provide an answer.

Accurate costs are random but near the target. For example, I have a refrigerator with a thermostat that keeps it a constant 38.0F. I test it with a dollar store thermometer 10 times. The temp readings range from 37F to 39F. Therefore, my inexpensive measurement system is accurate …close to the 38.0F target … but lacks precision.

Precise costs are repeatable but not necessarily accurate. Using the refrigerator example, an expensive scientific thermometer would have decimals and register precisely the exact same temperature during each of the 10 tests. The precise measure might be 36.05F after each of the 10 measurements or it could be precisely 38.05F each time. How could an expensive measurement system be consistently different? Not calibrating the measurement system before use is commonly the root cause.

Precise implies accurate but that assumption is wrong. Precise systems are more expensive than accurate systems but often not what we need.

You may be thinking “Why should I care?”

Short answer is “To have a profitable business, you’ve got to match the accuracy of your cost system to your type of business“.

Select the situation that best describe your business:

- Low Accuracy-Low Precision: If you’re the sole provider of a new product or service that delivers high value to customers, you don’t immediately need an accurate or precise cost system. Charge customers whatever price you want as long as net profits exceed 10%.

- Low Accuracy-High Precision: If you have competitors with published prices, you need a precise cost system. A precise cost system, like Activity Based Costing (ABC), will consistently enable you to define, implement and measure continuous improvement to eliminate waste and compete.

- High Accuracy-Low Precision: If you Bid & Quote for new business, you need an accurate cost system. If your bid is based on inaccurate costs, one of two things will happen; (1) your batting average on bids will be low; or, (2) you’ll win unprofitable orders you wished you hadn’t won.

- High Accuracy-High Precision: If you compete in a market that has excess capacity, you’ll need a precise and accurate cost system. An Activity Based Cost system works well here because it measures Non-Value Added excess capacity. To take sales revenue from competition, you may want to price your product or service based on a highly accurate cost that excludes the precise expense of excess capacity.

Barometric pressure is precisely useless information. It’s precise because it has two decimal points, e.g., 28.35. But to me it’s not accurate because I don’t know what the number implies, what I should do or what I should expect.

If your choice of cost system has your head spinning like barometric pressure does to me, give me a shout. I’ll help you match your needs to the best costing method.

]]>- Hold monthly ABM Show & Tell staff meetings. Select employees each month to discuss their activity procedures, output and cost performance. Feature new and previously enacted continuous improvement action plans each meeting. Celebrate the results!

- Use departmental ABM reports during annual employee performance reviews. Discuss which activities they would like to do more of (value) and which they would like to do less of (non-value).

- Print an ABC Bill of Activity for your most profitable product and least profitable product. Give copies to Marketing, Design Engineering or your R&D team. Show them how to read and use an existing product’s Bill of Activity to predict the cost of new products.

- Review your Top 10 most expensive Value-Added activities report. Select one to benchmark with a company outside your industry. Call ICMS for candidates.

- Name a process manager and process improvement team for one or more of your ABM business processes. Ask the process team to select one activity output from their process to measure daily. Chart this Key Performance Indicator on a greaseboard in a highly visible location.

- Review the Top 10 most expensive activities and Top 5 most expensive business processes during your annual strategic planning meeting. Do the activities and processes support the strategy or mission statement of the organization? Which of the activities or processes are your organizations core competencies? You’ll be surprised with the discussion and findings.

- Create an ABC Bill of Activity for a typical sales transaction for one of your most important customers. Hold a meeting with the customer. Use the report as a common language to discuss and define methods to mutually lower the cost of every sales transaction and split the savings.

- Link your ABM database to an Economic Value Analysis (EVA) model. Using a DuPont Model return on investment flowchart, identify specific activities and business processes that could significantly improve your EVA calculation.

- Review the most frequently produced ABM/ABC reports with a cross section of general management and employees. Ask them if they understand and use the reports. Use their constructive criticism to improve your ABM reports.

- Send a copy of one your departmental Activity Accounting reports to ICMS. We’ll quickly respond with a FREE benchmarking analysis.

If this article has inspired you and your organization to cut costs this year, call us at 817-475-2945, or e-mail your needs to tompryor@icms.net.

]]>This thought provoking statement by Zig Ziglar hits at the heart why many ABM implementations fall short of expectations. Many ABM champions spend all their project budget on software and consultants, leaving little or no resources to train employees “how to use” the new ABM information and reports.

While the principle of ABM is common sense….activities consume resources and products consume activities….ABM is not common knowledge in the non-financial ranks of your organization. To achieve and sustain meaningful ABM results, all managers and employees must eventually be trained “How to Read”, “How to Interpret” and “How to Use” ABM & ABC reports. ABM always fails in an organization if training is limited to the ABM Pilot Project team and the accountants.

ICMS offers on-line ABM and ABC training at www.LearnABM.com plus a variety of ABM and ABConsite workshops for your non-financial managers and employees. For example, here are a couple of our most popular courses:

ABM & ABC for the Non-Financial Manager…this comprehensive two day onsite workshop, led by ICMS expert trainers, will use your own activity accounting data to teach managers “how to” read, interpret and use their own ABM information. Are you tired of pushing ABM? After this workshop, managers will be pulling for more and more useful ABM information. An ICMS facilitator, using your facts, in a fun learning process will create fantastic results.

ABM Continuous Improvement Workshop…this 2 day workshop has become the most popular workshop in ICMS’s portfolio. Using your own ABM/ABC data, we teach both direct and indirect labor employees “how to” define, implement and measure cost reduction projects for their work area. Cost savings projects identified during this workshop will be presented to senior management for approval. Typically these cost savings projects provide a 10:1 payback on the ICMS workshop fees. Call ICMS at 817-475-2945 for more details, examples, and client references. One recent workshop client had this to say about the continuous improvement workshop……

“The workshops are professionally facilitated and have resulted in cost savings plans which are many multiples of your fee for services.” Fred Wszolek, FORD Motor Company

REMEMBER….Profits will not improve until every employee understands and uses ABM information on a regular basis. Call or e-mail us today to discuss your training needs… Phone: 817.633.2873 E-mail:tompryor@icms.net

]]>Over 90% of ABC Pilot Projects successfully demonstrate the principles and benefits of Activity Based Costing. Yet employees simply go back to business as usual right after the final project report is presented to senior management. What happened? During the 90 day pilot project everyone agreed that ABC is simply common sense e.g. activities consume resources and products consume activities. But on the 91st day the company returned to the customary management of direct versus indirect headcount, fixed versus variable cost accounts, and end-of-the month mentality.

Has your ABC/ABM implementation stalled out? Do you need to regain momentum and direction? Here are Five Steps to Jump-start your ABC Project:

Step 1 – Use a little bit of both ABM & ABC.

If your project has been totally ABC product cost focused, immediately add some ABM cost management steps. ABC product costing does not evoke employee emotion. You’re simply reallocating their cost. But ABM cost improvement does evoke employee emotion. Now you’re talking about changing their job or cutting their budget. Adding ABM to your ABC Pilot Project will get employees more interested and involved. Adding ABM to your ABC project will reduce costs!!

Step 2 – Eliminate bottlenecks.

A lot of ABC Pilot Projects stall out because of an information bottleneck. To eliminate your ABC Pilot Project constraints: (a) Don’t limit ABC training to the project leader and the cost accounting staff. Train a broad cross section of your employees “How to Read, Interpret and Use ABC reports”. (b) If only one person understands and uses your ABC software, you’ve got a bottleneck. Upgrade to a network or client server ABC system and train non-financial managers “How to Use” the system.

Step 3 – Want to be an ABC player? Get an ABC/ABM coach!

Hire an expert to motivate, provide positive examples, lead training and watch your application of ABC/ABM techniques. Pick a coach that matches your organization’s personality and industry type, with a plan that matches your goals.

Step 4 – Start a Productivity Patrol.

Post activity performance measures throughout the company. Remember the old saying “You get what you measure.” If your management wants ABC results on the company P&L statement, then you must develop highly visible performance measures that senior management can monitor as they walk around the company. To get results, activity and business process performance measures must be defined with positive and negative consequences linked to the achieving the targets. For example, Levi Strauss management during their 1995 ABM project launch defined a 28% product cost reduction target for 1998. The consequences were as follows: (a) miss the target and your plant will be closed; or, (b) hit the target and every employee receives one year’s salary as a bonus. Would these consequences “jump-start” your employees?

Step 5 – Listen to your customers.

Bring in a supplier or customer that has successfully implemented ABC. People like to hear success stories. Especially if they are examples from someone they know and respect. Have your supplier or customer share their ABC excitement with your employees. Discuss how you and they could mutually benefit by using ABC to synchronize processes, benchmark common activities, eliminate waste, and grow both businesses.

The only thing worse than having a failed ABC Pilot Project is completing a successful ABC Pilot Project and watching it stall out.

Don’t be an ABC dropout and let your hard work go to waste. Try these Five Steps to jump-start your project. If you need any help or additional ideas, simply give us a call at 817-475-2945. We are here to help you.

]]>The first atomic bomb was mostly TNT packed around a tiny bit of U235. The TNT imploded into the U235 causing an “atomic reaction” which then exploded outward. The atomic bomb is a model for creating a large and lasting change in an organization. If you want something big, “explode” a pile of TNT. But if you want something really big, use your TNT to “implode” on a small bit of “Critical Mass” and let that do the exploding later.

The Bible provides us an example of how one man focused on a critical mass of twelve to create a sustainable success. In the book of Matthew, Jesus imploded His teaching, vision, burden, and call on a small group of twelve disciples for three years. In the book of Acts we read about the creation of the church by those disciples after Jesus’ death. The chain reaction explosion of their work continues today. Over 2,000 years later.

Critical Mass argues for starting with a core not a crowd, a small group not a convention, leaders not the masses. This model argues that people who really want to leave behind a massive chain reaction “spend more time with less people to achieve greater results.”

Activity Based Management (ABM) has provided a huge positive impact on many organizations during the past ten years. Without exception, each of those organizations had an “ABM Critical Mass” from the onset.

- At the core of your critical mass is a knowledgeable champion of ABM and ABC. Someone who not only understands the principles of ABM but also how important ABM is for meeting the needs of the organization. This person is likely a “disciple” of an outside ABM expert.

- Surrounding the champion is a senior management team. They provide the positive “charge” to the explosion. While they too must understand ABM, their primary role is to provide direction and resources to implement and sustain ABM. They define the ABM performance measurement goals coupled with the positive or negative consequences of achieving those goals. At a minimum, provide your senior management a ½ day overview of ABM.

- Last but not least, surrounding the critical mass are employees who can provide positive testimonials to the benefits of ABM. These are employees who have used and benefited from ABM. They spread the “gospel” of ABM both internally and externally. They should be nurtured with ABM books, articles, coaching, trainingand direction. And don’t forget to celebrate with them. Celebrating the benefits of ABM adds punch to performance.

Are you a part of the critical mass in your organization? If not, you can be. I look forward to hearing from you at TomPryor@ICMS.net.

]]>Many people are familiar with ABM and ABC. But “knowing about ABM” is not the same as “knowing ABM”. Reading a book on marriage is not the same as spending time with one’s spouse. Knowing someone’s phone number is a far cry from enjoying friendship with that person. Knowing about God is much different than knowing God.

Here are questions that you and your organization could expect from an interrogator to determine if your ABM involvement is circumstantial or convicting:

- Can you and every member of your senior management team explain the basic principles of Activity Based Management?

When I worked at Motorola during their successful journey to achieving six-sigma quality (3.4 defects per one million), every manager could explain the principles and benefits of Total Quality Management in five minutes of less. If your management team does not understand ABM, how do you ever expect the employees to embrace and use it? Has your senior management team been trained “how to” read, interpret and use ABM reports? If not, why not?

- Do you consistently issue monthly or quarterly ABM reports?

Repetition is a requirement for competency. If I play golf only 1 or 2 times per year, I will not remember the rules or the best techniques to optimize and enjoy my game. Organizations that have been the most successful with achieving benefits with ABM have made activity measurement a regular routine. Regular measurement is a strong indication of your commitment to ABM. If you want activity cost improvement, you must repeatedly measure activity performance. Keep a journal of ABM success stories in your organization. If you cannot point to positive, quantifiable results from your ABM system, you will not be convicted.

- Do you hang out with other ABM’ers?

The February 16, 1999 issue of USA TODAY reported that 73% of Americans say that religion is an important part of their life but only 12% of those people surveyed attend church weekly. Being with other believers on a regular basis keeps you committed, encouraged and accountable. Attend at least one ABM conference per year. Form a local ABM User’s Group in your city. I hear of many groups forming. And develop an E-Mail chat group with fellow ABM’ers. E-Mail is great for problem solving and benchmarking.

Knowing about ABM is circumstantial evidence. Take steps today to make sure you and your organization is convicted.

]]>Most of us spend the first half of our life focused on success. Achieving a successful career, a successful marriage and the like. Mr. Buford recommends that we spend the second half of our life focused on significance. e.g. What will be your epitaph? What do you want to be remembered for? Most Activity Based Management (ABM) implementations experience a similar mid-life, halftime crisis.

Halftime in an ABM project usually occurs right after the implementation team has successfully defined the activities and loaded the ABM software with costs, workload measures and non-value labels. As ABM software reports come spewing out of the printer, the team often looks at the project leader and asks, “Is that all there is to ABM?” The answer to that question and the decisions made at halftime determine whether ABM will have a significant financial impact on an organization.

How do you transition from the successful creation of an ABM software model to the significant benefits your organization desires? You have four choices at ABM halftime. Only two will provide the significant benefits that your organization likely desires:

- A small change to a small activity is a waste of time.

- A big change to a small activity is an illusion of progress.

- A small change to a big activity is the embodiment of continuous improvement.

- A big change to a big activity is a big payoff.

What is the best choice for your organization? In an organization that already practices continuous improvement techniques, option #3 will significantly convince employees that ABM is a valuable tool that supports, optimizes and sustains cost improvement. On the other hand, organizations that need a big wow should choose option #4. This option will significantly impress any employee who is cautiously optimistic about the potential benefits of ABM. Both #3 and #4 will have a positive impact. Your senior management and employees will be the jury that determines if the activity change was big enough to be judged significant.

Halftime in any sporting event is used by the players and coaches to assess the positive and negative events of the first half. Before the second half begins, a consensus plan is developed outlining the changes and adjustments necessary to win the game. Take a personal and professional halftime this year to make sure your legacy is significant.

]]>- I can name my spouse’s best friends.

- I can tell you what stresses my spouse is currently facing.

- I can tell you some of my spouse’s life dreams.

- I know the names of some of the people who have been irritating my spouse lately.

- I can tell you about my spouse’s basic philosophy of life.

- We love talking to each other.

- There is fire and passion in our relationship.

- At the end of the day my spouse is glad to see me.

- My spouse is one of my best friends.

- My spouse is usually a great help as a problem solver.

Give yourself one point for each true answer. If you scored above 6 or more, Mr. Gottman predicts that you have the makings for a strong marriage. If 5 or below, your relationship could stand some improvement and would benefit from some work on the basics, such as improving communication.

How strong is your marriage to Activity Based Management (ABM)? Are you and your organization madly in love with ABM or close to a divorce? Answer each of the following ten statements with a “True” or “False”:

- My organization has sustained regular ABM reporting for more than twelve months.

- I can explain the basic principles of ABM in three minutes or less to a non-financial person.

- I can name at least two significant benefits my organization has achieved in the past year using ABM.

- I can name our most profitable and unprofitable product, service and customer exposed by Activity Based Cost (ABC) analysis.

- I know the improvement target for my activities and the continuous improvement steps to achieve that target.

- I can name the customers of the outputs of my department’s activities.

- I can name at least one person that I have mentored and passed along my ABM knowledge and experience.

- I own at least two books on ABM or ABC.

- I know how to do Activity Based Budgeting.

- I know and talk regularly with at least one other person outside my company who has an ABM system.

Give yourself one point for each true answer. If you scored 6 or more, I predict that you and ABM have the makings for a strong marriage. If 5 or less, your relationship could stand some improvement and would benefit from some work on the basics.

My wonderful wife of 30+ years reminded me last year that husband is both a noun and a verb. I am a husband (noun). But to be called a husband, I must husband (verb), e.g. perform activities that are the responsibility of the husband. Tony Evans says in his book NO MORE EXCUSES that when the average man is asked, “Do you know the responsibilities of a husband?”, they respond “I don’t know” or will give an answer that reveals they don’t know. You must know (noun) before you can do (verb). The same issues apply to Activity Based Management.

As discussed in my book PRYOR CONVICTIONS, ABM is also a noun and a verb. ABM is not just a system or body of knowledge (noun). ABM is also a verb e.g. perform activities, implement improvements, make decisions. The ten ABM questions listed above are a test to determine if ABM is both a noun and verb in your organization. To have a strong marriage, it takes both a noun and a verb. Know it and do it.

As it has been often said about marriage, “Two heads are better than one.” Or as President Woodrow Wilson said, “I not only use all the brains I have, but all I can borrow.” To strengthen ABM and its benefits in your organization this year, add some brains. Consider some targeted ABM training to fill knowledge voids or specific requests from ABM system users. Expand the breadth and depth of ABM in your organization. Or maybe some onsite ABM coaching from a seasoned and successful ABM consultant would be a logical next step. And don’t forget that over forty books on ABM principles, uses, case studies and techniques are available to increase your knowledge and imagination.

Don’t settle for less than “10” in marriage or ABM. Take steps beginning today to improve your marriage and make ABM a lifelong partner.

]]>Alexander Graham Bell:

“Do you want to buy a telephone?”

First Customer:

“What’s a telephone?”

Alexander Graham Bell: “It’s a thing that you can use to call other people.”

First Customer:

“Does anyone else own a phone?”

Alexander Graham Bell: “Not yet. You’ll be the first.”

First Customer:

“If that’s the case, then I think I’ll wait until there is someone else that I can call.”

The first phone had no value. The second phone had significant value because it made the output of the first phone useful. As each additional phone was sold and added to the network, the value of all phones increased exponentially.

If you own PC-based Activity Based Management (ABM) software, with a single data set, created by a lone individual, you have something in common with Alexander Graham Bell. One is a lonely number. To achieve success, you both need more than one customer. Additional users of the ABM software are needed to exponentially add value to any organization. One PC model with one user represents a significant constraint to optimizing and sustaining the full value of ABM.

Bottleneck #1: ABM software is installed on a single PC. ABM software is frequently installed on a desktop or laptop PC. While this approach is initially very practical, it will eventually become an obstacle to efficient information flow. A standalone software model restricts the flow of ABM data and reports to other employees. Employees that have no ready access to the ABM data cannot make timely, relevant decisions or measure performance improvement. Gaining access to the lone PC makes updating the activity cost for new time periods cumbersome and frustrating.

Solution: Install PC-licensed software on the network file server or purchase a network license with multiple user nodes.

When purchasing ABM software, most organizations opt for the lower priced PC license. Without thought, the software is often installed on a desktop PC, thereby limiting the number of people who can access the system. Why not install the PC-licensed software on a network file server?

While most ABM/ABC software products offer both PC and multi-node network licenses, it is often not practical to purchase the more costly network version when first launching ABM in a company. Network licenses provide the capability of simultaneous use of the software by more than one person. PC licenses allow only one user at a time. But installing a PC license on a file server provides the immediate flexibility of being able to access the ABM software from any PC on the network. Select a solution that best meets your needs and budget.

Bottleneck #2: Having only one trained software user. The individual who creates the ABM software model is often the only person who fully understands ABM and the software system’s reporting capabilities. Because a lone individual has limited time and resources, that person quickly becomes a constraint to optimizing and sustaining the benefits of ABM. When only one person is available to update and use the software, they have little or no time to ask and answer ABM questions.

If the person who created the ABM software model leaves the organization, no one will be left to use or maintain the data. People with hands-on ABM experience are in much demand today in the labor marketplace. A talented person with significant ABM experience can easily command $75,000-$100,000 as an ABM consultant or corporate Director of ABM.

Solution: Provide software training to several people and have them use the software regularly.

While training several people on the software is often not practical at the onset, training should be an immediate consideration after completion of a successful ABM Pilot Project. Train people that will use the ABM software data frequently during the context of their regular job duties, e.g. accountants, industrial engineers, information systems managers, process improvement manager, etc. Three training resources exist: (1) have the employee who created the initial model cross-train other employees immediately after the pilot project; (2) have employees use a self-paced tutorial from the software vendor; or, (3) use expert trainers from the software vendor to train employees.

Bottleneck #3: Inadequate ABM training of non-financial managers. The individual who creates and maintains the software model is often not capable of training other employees on the principles and uses of ABM. He or she does not have the time or talent to train others on “how to” read, interpret and use the ABM software reports for decision-making or continuous improvement. As a result, the valuable data that has been created in the ABM system goes unused. Senior management needs ABM training and coaching. Middle management needs ABM training and coaching. Eventually all employees need to be trained and coached how to use ABM to meet their needs. ABM training is now available on-line. Check out www.LearnABM.com and take a sneak preview at on-line ABM learning.

Solution: Provide “how to use ABM” training to all employees.

Best selling author and motivational speaker John Maxwell says “Don’t let your learning lead to knowledge, let your learning lead to action.” Provide employees hands-on ABM training. Show them how to use their own activity accounting reports to define, implement and measure improvement action plans for their department.

Training that uses generic ABM examples or case studies do not convince skeptical employees that question the principles and benefits of activity measurement. Adults, however, rarely argue with their own data. Therefore, training that combines “older” and proven continuous improvement techniques with the “newer” ABM data works best. The three most common options companies use to train non-financial employees are: (1) provide each employee a copy of the book Using ABM for Continuous Improvement workbook and require them to submit to senior management for approval an activity cost improvement action plan; (2) hire an experienced ABM trainer to provide an onsite workshop using your actual ABM data; or, (3) designate one or more qualified people in your organization to train and coach other employees on the proper use of ABM data.

Conclusion Paul Strassmann, instrumental in introducing ABM to the U.S. Department of Defense during the Bush administration, says, “The excellent executive cannot be considered to be productive if the rest of the organization cannot translate his intentions into results.” Strassmann emphasizes in his book, Information Payoff, “the productivity of management must be measured by its performance as a team, rather than by summing up individual efficiencies.”

One PC-based ABM software model with a lone user will not result in lasting efficiencies. Building a team of knowledgeable ABM users is absolutely imperative if maximum ABM benefits are to be achieved in any organization. Make ABM data and knowledge readily available to everyone that needs it. Don’t allow anything or anyone, especially yourself, to be the constraint that restricts the effective use of ABM in your organization.

]]>